Understanding how to evaluate a company’s financial condition is an essential skill for both accountants and potential investors. One way to value a company is to analyze the carrying value of its assets. It is important to distinguish between net book value and similar concepts such as market value and book value.

In this article, we define book value . We will show you how to read balance sheets to determine the net value of assets, companies, and stocks.

Key ideas

- The total amount that a company would earn if it liquidates without selling assets at a loss represents the carrying value of a company.

- Accounting value is not the same as value. However, both are methods of valuing an asset.

- The Accounting value of a company is usually less than its market value.

What is a Book Value?

Book Value is the total number of assets subtracted by the total number of liabilities. As simple as that. It helps in calculating the valuation of an organization.

How to calculate book value of an Organization?

A Company is calculating simple net value by subtracting total liabilities from total assets. we can call it as the net value of equity. More detailed book values take other factors into account, such as the deduction of intangible assets.

For example, a company has assets of INR 2,000,000 and liabilities of INR 5,000,000. The Accounting value of the company is ₹2,00,00,000 – ₹5,00,000 = ₹1,50,00,000/-.

That means. Book value of a company = total assets – total liabilities

How to calculate book value of assets?

To calculate net Accounting value for tangible assets subtract depreciation from the original cost. If assets require additional improvements, Add the cost to its original cost.

For example, The Cake Company bought a box-making machine for ₹11,000. After five years, the machine has depreciated at a rate of ₹1000 per year (using straight line depreciation). Its Accounting value is now ₹6000.

BVPS

BVPS is the book value per share. Investors calculate the balance sheet of a company that interests them. Investors can compare the BVPS to a stock’s market price to get an idea of whether that stock is overvalue or undervalue.

To obtain BVPS, total common stockholders’ equity divide’s by the total number of common shares outstanding. To get the common shareholder’s total equity number, take the total equity number and subtract the value of the preferred shares. If there are no preferred shares, simply use the total share capital.

BVPS = Total Shareholders’ Capital – Preference Shares / Total Common Shares Outstanding

So if a company had ₹20,00,00,000 equity capital (and no preference shares) and ₹10,00,000 common shares outstanding, its book value per share would be ₹200/-:

BVPS = INR 20,00,00,000 / 10,00,000

BVPS = INR 200

If the market price of a stock is higher than the BVPS, then the stock consider overvalued.

There is a difference between outstanding and issued shares, but some companies may refer to outstanding common shares as issued shares in their reports.

Importance of Book Value

Now that you are familiar with the importance of Accounting value, let’s take a look at some reasons why book value is important.

- Asset Valuation: Net value provides an accurate assessment of a company’s assets and liabilities, giving investors a clear understanding of the company’s financial condition. By subtracting liabilities from assets, investors can determine the company’s net worth.

- Investment decision: Accounting value can be use to evaluate the potential profitability of an investment. If the market value of a company’s stock is less than the book value per share, it may be an indication that the stock is undervalue and represents a good investment opportunity.

- Liquidity assessment: Accounting value can help investors evaluate a company’s ability to meet its financial obligations. When the Accounting value of a company’s assets exceeds its liabilities. It indicates that the company has positive net worth and is financially stable.

- Risk Management: Net Carrying value can be used to determine the risk associated with an investment. A company with a high Carrying value per share is generally considered less risky than a company with a low Carrying value per share.

Limitations of Book Value

Now that you’ve learned the definition of book value, take a look at some limitations of it.

● Periodic Publication: Calculate net value typically and publish periodically, such as quarterly or annually. This means it may not reflect the current market value of a company’s assets and liabilities.

● Historical Cost: Net asset value calculate using historical costs, which may not reflect the current market value of a company’s assets. This can lead to an inaccurate assessment of the company’s value.

● Not applicable for labor-intensive companies: The net value does not take into account intangible assets such as a company’s workforce or intellectual property. This can be a significant limitation for labor-intensive companies where the value of the company’s workforce is a significant factor in its overall value.

● Sector-specific limitations: Carrying value may not apply to companies operating in certain sectors, e.g. B. in the technology or pharmaceutical industries. In this the value of the company’s intellectual property and research and development activities can be an important factor in its overall value.

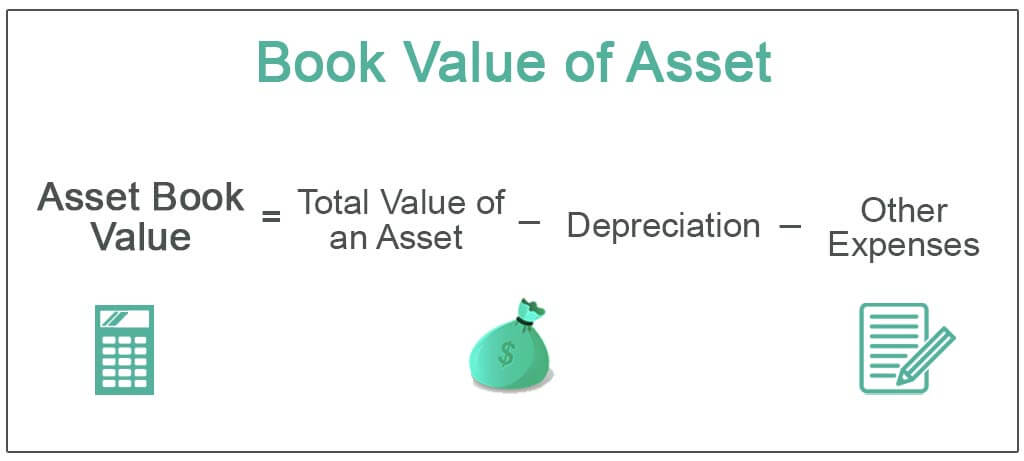

Asset Book Value

The initial Net asset value of an asset is its actual cash value or cost. Cash holdings record or “account” at their actual cash value. Assets such as buildings, land and equipment are value based on their historical cost. It is the actual cash cost of the asset plus certain costs associate with purchasing the asset, such as: Brokerage fees include, Not all items purchased are recorded as assets; Additional services record as expenses. Some assets may record as current expenses for tax purposes.

Depreciable assets: Depreciable assets are assets that lose value over time due to wear, use, or obsolescence. They can be tangible, such as machines, vehicles or office buildings, or intangible, such as patents, copyrights or computer programs.

Amortizable assets: Depreciation is an accounting technique used to periodically reduce the net value of a loan or intangible asset over a period of time. Depreciable assets have no physical presence.

Depletable assets: Depletable assets are resources that are depleted or cannot be produced as quickly as they are consumed. Examples of exhaustible assets include: oil reserves, forests, mineral rights, coal, gold, iron ore and copper.

Price-to-Book (P/B) Ratio

The price-to-book (P/B) ratio is a valuation multiple that can be used to compare the value of similar companies within the same industry. However, it is important to remember that this ratio may not serve as a valid valuation basis for comparing companies from different industries and industries.

This is because companies may use different accounting methods to determine the carrying value of an asset. Some companies record their assets at cost, while others value their assets at market price. Therefore, a high price-to-book ratio does not always indicate a premium valuation and a low price-to-book ratio does not necessarily indicate a discounted valuation.

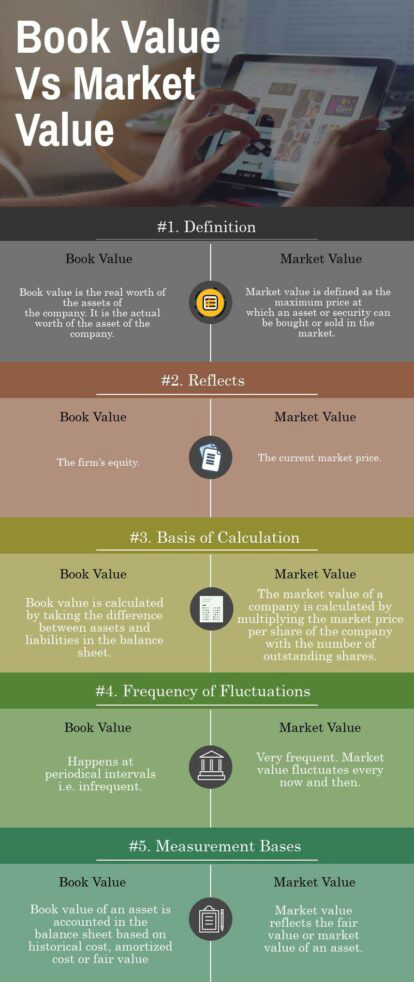

Book Value versus Market Value

Investors have many metrics to determine the valuation of a company’s shares. Most commonly used metrics are Net asset value and market value. Both can be helpful in calculation whether a stock is fairly value, overvalue, or undervalue. In this article, we will look at the differences between the two and how they are used by investors and analysts.

Easy to remember points:

- A company’s carrying value is the amount of money that shareholders would receive if assets liquidates and liabilities pays.

- Market value is the market value of a company based on the current share price and the number of shares outstanding.

- If market value is less than Net asset value, the market does not believe the company is worth its Net asset value.

- A higher market value than Net asset value means that the market places. A high value on the company due to expected increases in profits.

- When using Net asset value and market value to compare companies, it is important to compare companies within the same industry.

Book Value vs. Carrying Value

Companies own many assets and the value of these assets is derives from a company’s balance sheet. There are different ways to value and record an asset. However, the most common method is to take the purchase price of the asset and subtract its depreciation costs. This represents the Net asset value .

For all intents and purposes, the two terms are interchangeable. The term “book value” derives from the accounting practice of recording the value of an asset based on its original historical cost less depreciation. Net asset value analyses the value of an asset over its useful life; a calculation that includes depreciation.

Net asset value can refer to several different financial metrics. While carrying value uses business accounting and is typically distinguish from market value. In most contexts, Net asset value describe the same accounting concepts. In these cases, the difference lies mainly in the type of companies each uses.

Conclusion

Book value is a financial ratio used to determine the value of a company. However, investors should be cautious about relying solely on it as it may not fully represent all aspects of a company’s assets.

GTjafLqAsqoUoSLGgXtGkN

Your comment is awaiting moderation.